The Forgiveness Problem

The President’s executive order to forgive up to $20,000 of student debt per borrower may be seen as a long-overdue benefit that college graduates deserve, or an inflation-feeding monster that will enlarge the federal deficit, resulting in higher consumer prices, or a small gesture that falls short of the elaborate promises made to erase outstanding student debt. The action is in fact all of these, and less.

One of the biggest complaints about loan forgiveness, is that it contributes to inflation. All government spending can do this. The total expense of loan payments, spread out over many years, however, means that these loans are not likely to have a measurable effect on inflation. The effect of loan forgiveness on inflation pales in comparison to the effect of the massive amount of money printed by the Treasury in the past years. It does, however, more than erase all of the deficit savings from the recent “Deficit Reduction Bill.”

This debt erasure does create several real problems, highlighting fundamental issues with the federal student loan program in general. Let’s explore some of the major concerns:

The loan forgiveness is weighted towards upwardly mobile white students who already earn more than people of color and are on track to continue to out-earn the average American. The executive order Biden signed targets individuals earning up to $150K in annual income and $250K for couples. Whoever chose $250K a couple as a maximum benchmark had voters in mind, not low-income students.

The forgiveness is fundamentally unfair. Millions of Americans, myself included, have paid off their federal loans. If they accomplished this prior to Covid, they receive no financial benefit. If a student takes out a federal student loan or accepts a Pell grant next week, they receive no forgiveness in this plan. If the student was unlucky enough to borrow money from family, friends or a private financial institution, then they still owe every dollar on their student loan.

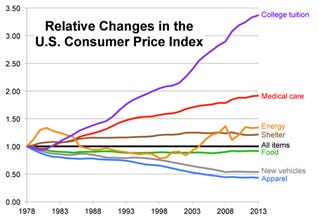

Federal loans contribute to soaring education costs. Easy government money is a major factor in making education costly in America. Just as endowments power higher spending by schools, government loans and grants have made universities comfortable with charging more. The cost of higher education has outpaced almost every other type of cost in the United States. (Source: Mybudget360.com) This executive action will contribute to already out-of-control costs of higher education. In the long run, these rising costs will hurt far more low-income students than the action has helped.

The action is possibly illegal. Biden knew this when he told a CNN Town Hall that “I don’t think I have the authority to do it by signing with a pen.” Even House Speaker Pelosi got it right the first time when she said, “People think that the President of the United States has the power for debt forgiveness,” she said. “He does not. He can postpone, he can delay, but he does not have that power. That has to be an act of Congress.” When the two most powerful people in government acknowledge that an action is not legally possible, we have to ask what has changed. What could be behind this flip-flop?

Not the American people, who, by and large, oppose this hand-out. A CNBC poll showed that the majority of Americans were concerned that erasing student loan debt would exacerbate inflation. Only 34% felt that those in need deserved forgiveness, and even less were in favor of total debt cancellation. The giveaway is targeting two groups. First, upwardly mobile voters who may be influenced to vote for the President’s party in November. Second, the vocal minority in his party that has been calling for complete erasure of all student debt (no matter who issued it) and while we are at it, free higher education.

Even if this is legal, this continues a terrible precedent of out-of-control Executive Action. Presidents have increasingly dashed off ill-thought-out executive actions, often using extremely convoluted rational. In the current case, the debt forgiveness is related to an ‘emergency’ stemming from the pandemic. Like all executive actions, this one has nothing to do with law-making, and can be reversed by a future president with the stroke of a pen.

The action diverts attention from actual low-cost colleges. State colleges, many of them excellent, have low-cost tuition available in many states. There are also many free 2- and 4-year colleges to choose from. This action doesn’t encourage and expand the offering of the dozens of affordable schools that already exist. Instead Biden’s action rewards students for getting loans for expensive institutions, many of them overpriced, given their increasingly lackluster results. Forbes reports that less than 60% of college students earn a bachelor’s degree, even after 6 years!

Is this really an ‘emergency’? As a recipient of a forgiven small-business Paycheck Protection Program loan, I acknowledge that these loans contributed to our current inflation woes. The PPP program differs from the student bail-out in significant ways. For one thing, small business shutdowns were related to real emergencies that were arguably exacerbated by incompetent government responses. Also, unlike the student giveaway, PPP applied to virtually all small businesses, not a small segment of motivated voters. The guidelines for forgiveness were clearly laid out from the start, not applied by executive whim.

We are perpetuating, not solving, a major problem. The real question that we should be asking is why the federal government is in competition with the private financial sector. Washington issues loans and provides insurance that is already competently handled by the private sector. Like flood insurance, however, some will point out that if the US government did not provide it to consumers, then people could not obtain it affordably. At this point, taxpayers are on the hook for an amazing 92% of all college loans!

The answer to that point, of course, is that if a bank or insurance company feels that a business is too risky, then it does not follow that the taxpayers should instead assume the costs of those risks. I cannot imagine a less competent issuer of loans than the federal government. The Government Accountability Office (GAO) agrees.

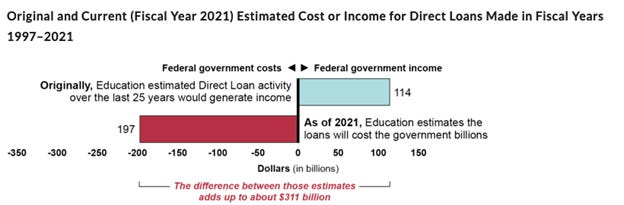

The Education Department had projected the government student loan program to earn an income of $114 billion (essentially gaining 1% net interest after loan expenses, based on estimated pay back schedules) on loans made over the past 25 years. Who out there is shocked to learn that the GAO now predicts a loss of $197 billion on those same loans? In fact, the swing from profit to loss amounts to a $311 billion shortfall, according to the GAO’s own chart.

If a loan is a bad idea for a financial institution, it’s a bad idea for the taxpayers. Of all the efforts that can be made to increase the availability of low-cost colleges, as well as highlight great alternatives to college degrees, loaning college students’ money that they will not pay back gives us a very poor return.

Nancy Pelosi had it right the first time. Making laws resides in the halls of Congress, not with a ballpoint in the oval office. We need our representatives to acknowledge that the federal student loan program has been an ill-conceived money loser that has just been made dramatically worse with a single executive action. A willing private sector, and excellent low-cost schools can work together to offer affordable higher education.

We can stop repeating the mantra that everyone benefits from getting a degree. 40% of students already realize they are wasting their time graduating. Is there really any need to list the hundreds of high-profile college dropouts that have built our most successful businesses?

Congress needs to act to address the federal student loan program and the unintended consequences of market manipulation that it has created. If support is needed, then let’s focus on those truly in need of help. We need not provide handouts to well-to-do kids to court votes. If the president fears losing congressional seats this fall, let him buy those votes the old-fashioned way, with USDA certified Pork Projects. My district is in need of some new bridges to nowhere.